There are only two paths left for software

TLDR

- David George (a16z) argues every software company must now choose: accelerate revenue growth 10+ points via AI products, or rebuild to 40%+ true operating margins including stock-based compensation.

Key Takeaways

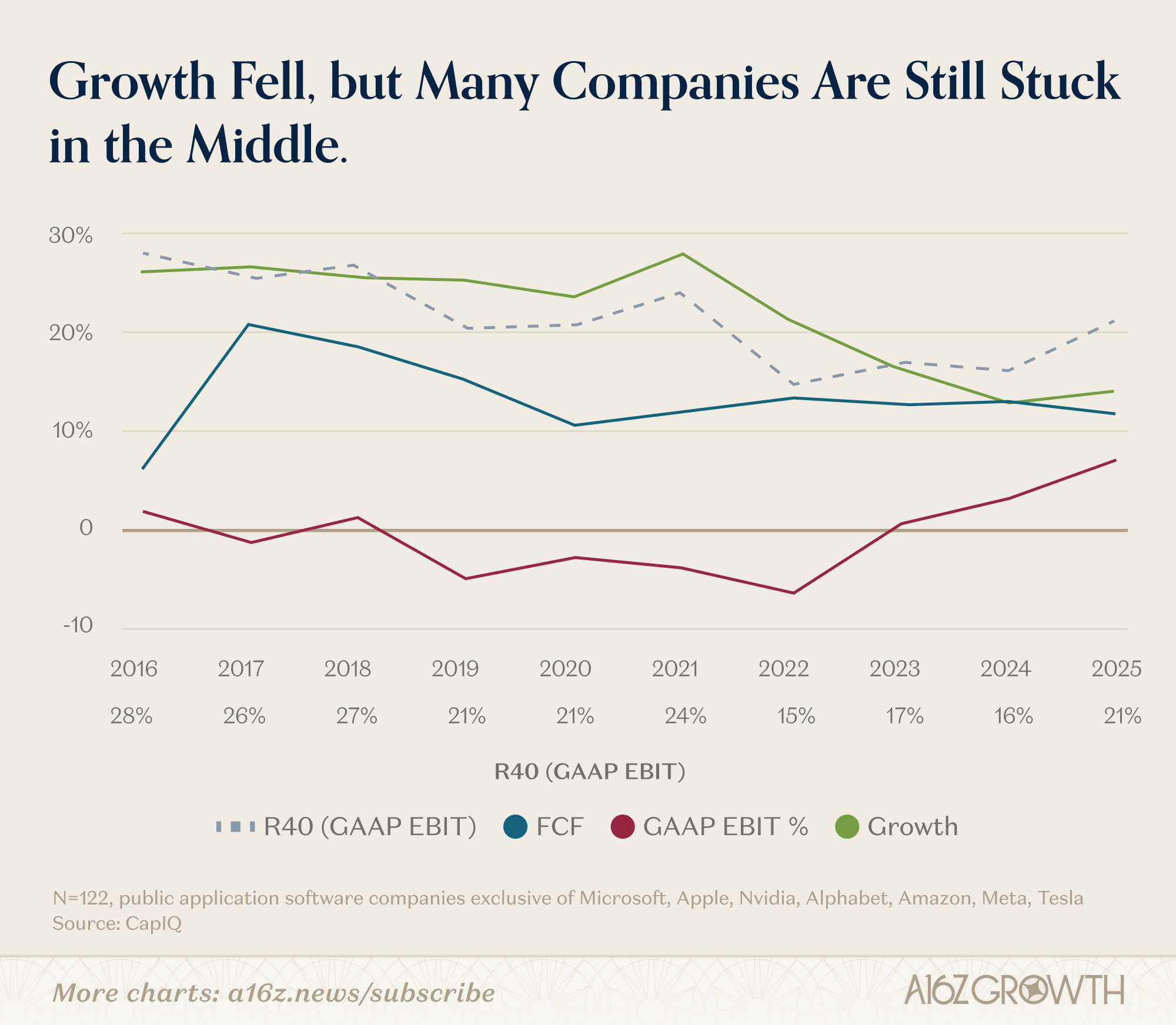

- The “comfortable middle” is over: companies too slow for a growth multiple and too diluted for a fortress multiple face multiple compression and persistent dilution.

- Path one demands net-new AI products that move total company growth rate by 10 percentage points within 12 months, not chatbot bolt-ons to existing SKUs.

- Path one requires a company rebuild: four-person pods, 50% of R&D on new products, token-based pricing replacing seat-based models, and a refreshed exec team within 30 days.

- Path two targets 40-50%+ true operating margins including SBC within 12-24 months, requiring flattened management layers, product stack cuts, and price realization on owned workflows.

- Broadcom’s acquisition and restructuring of VMware, reaching guided fiscal 2024 adjusted EBITDA of 61% of revenue, is cited as the only public-market proof the strong form of path two is achievable.

Why It Matters

- Public markets have already repriced software terminal value downward; free cash flow improvements have not translated to true profitability once stock comp is treated as a real expense.

- The board question George prescribes is binary: “+10 points of revenue growth from net-new AI products” or “40%+ true operating margins including SBC” – anything between is no-man’s land by end of 2026.

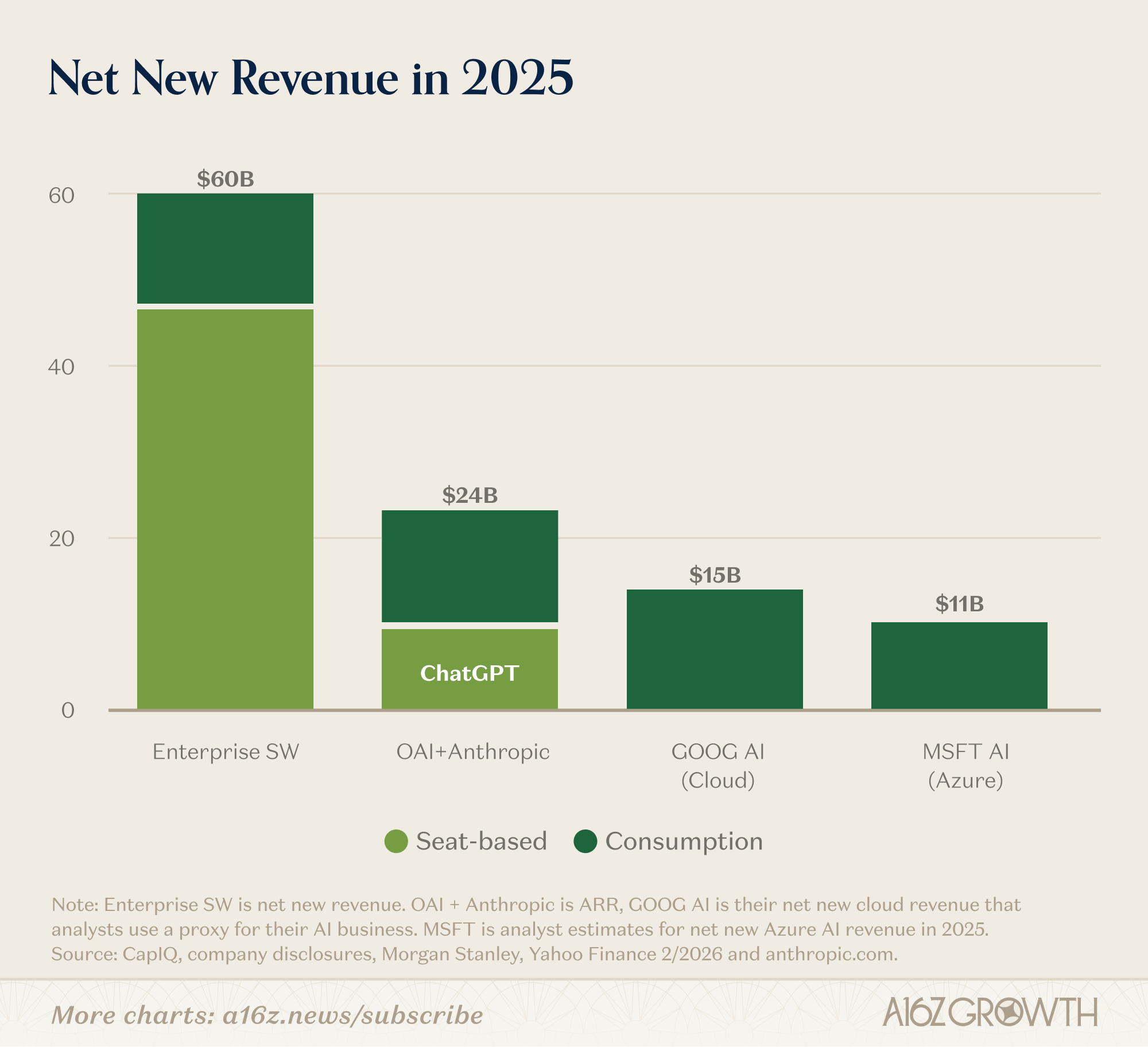

- Token and consumption pricing is where new software budget growth sits; seat-based cost cuts are where customers will look first, compressing legacy revenue simultaneously.

David George, Andreessen Horowitz · 2026-03-23 · Read the original